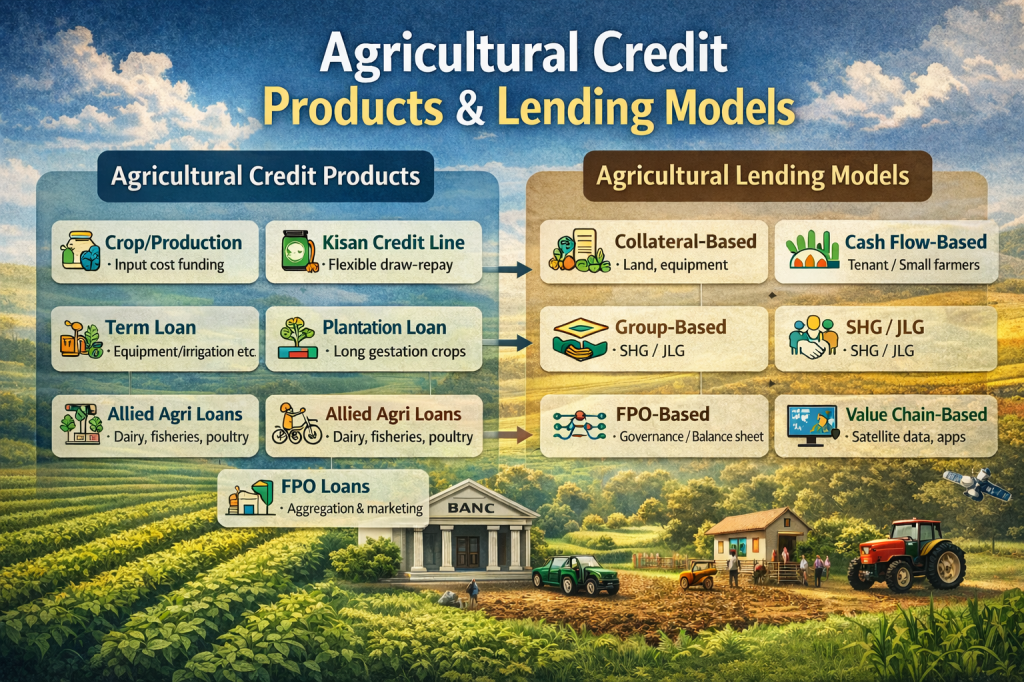

(How money actually flows to farmers, FPOs & agri-ecosystems)

1️⃣ Agricultural Credit Products

👉 “What type of loan is given?”

🔹 A. Crop / Production Loans (Short-term)

Purpose

- Seeds, fertilizers, pesticides, labour

- Seasonal working capital

Key characteristics

- Tenure: 6–12 months

- Repayment: After harvest

- Interest often subsidised

Analytics angle

- Yield risk

- Price volatility

- Weather exposure

- Repayment depends on one crop cycle

📌 Most common agri loan in India

🔹 B. Kisan Credit Line–Type Revolving Credit

Purpose

- Flexible credit for recurring farm needs

Key characteristics

- Revolving limit (like OD/CC)

- Draw–repay multiple times

- Based on landholding & cropping pattern

Analytics angle

- Utilisation pattern

- Repayment discipline

- Cash-flow smoothing

📌 Good dataset for behavioural credit analytics

🔹 C. Term Loans (Medium / Long Term)

Purpose

- Tractors, irrigation systems, plantations

- Dairy, poultry, farm mechanisation

Key characteristics

- Tenure: 3–7 years

- EMI-based repayment

- Asset-backed

Analytics angle

- Asset productivity

- Long-term income stability

- Default risk increases with climate shocks

🔹 D. Plantation Crop Loans

Purpose

- Coffee, tea, rubber, cardamom, spices

Key characteristics

- Long gestation period

- Moratorium before repayment

- Highly climate & price sensitive

Analytics angle

- Yield variability

- Price cycles

- Cash-flow gaps

📌 Perfect use case for risk analytics + insurance integration

🔹 E. Allied Agriculture Loans

Purpose

- Dairy, fisheries, poultry, beekeeping

Key characteristics

- Regular cash inflows

- Shorter cycles than crops

Analytics angle

- Daily/weekly cash flows

- Input price risk

- Disease risk

🔹 F. FPO / Agri-Enterprise Loans

Purpose

- Aggregation, processing, storage, marketing

Key characteristics

- Balance-sheet driven

- Governance risk

- Member dependency

Analytics angle

- Portfolio risk

- Operational risk

- Working capital cycles

2️⃣ Agricultural Lending Models

👉 “How does the lender decide & disburse?”

🔹 1. Collateral-Based Lending

Logic

- Land, equipment, warehouse receipts

Strength

- Lower credit risk for bank

Limitation

- Excludes small & tenant farmers

Analytics focus

- Collateral valuation

- Loan-to-value (LTV)

🔹 2. Cash-Flow–Based Lending (Emerging & Important)

Logic

- Repayment capacity > asset value

Uses

- Tenant farmers

- Smallholders

- FPO members

Analytics focus

- Crop-wise cash flows

- Stress scenarios

- DSCR

🔹 3. Group-Based / Joint Liability Lending

Logic

- Social collateral

- Peer monitoring

Used for

- SHGs, JLGs

Analytics focus

- Group default behaviour

- Correlation risk

- Contagion effects

🔹 4. Value Chain / Contract-Based Lending

Logic

- Linked to buyers, processors, exporters

Example

- Coffee buyer guarantees purchase

- Loan recovered from sale proceeds

Analytics focus

- Counterparty risk

- Price assurance

- Supply chain dependency

📌 Lower default, higher data dependency

🔹 5. Digital / Alternative Credit Models (Agri-FinTech)

Logic

- Data-driven decisions instead of land records

Data used

- Satellite data

- Transaction history

- Weather & yield proxies

Analytics focus

- Credit scoring

- Model explainability

- Bias & data gaps

📌 Future-ready but risky if misused

3️⃣ Simple Frame

Credit Product = Why money is borrowed

Lending Model = How risk is assessed & managed

4️⃣ Quick Mapping

| Credit Product | Lending Model | Key Risk |

|---|---|---|

| Crop loan | Cash-flow based | Yield & price |

| Plantation loan | Moratorium-based | Climate |

| FPO loan | Balance-sheet based | Governance |

| SHG/JLG | Group-based | Contagion |

| Contract farming | Value-chain based | Buyer risk |

Leave a comment